What Does Portfolio Strategy Mean in Commercial Real Estate?

Commercial real estate ownership often begins with a single property. A retail strip center purchased decades ago. An industrial building acquired for stable income. An office property inherited or developed.

Over time, however, many owners accumulate multiple properties, either intentionally or organically. Yet even when holdings expand, decision making frequently remains focused on one asset at a time.

This is where portfolio strategy enters the conversation.

Portfolio strategy in commercial real estate is the disciplined practice of evaluating properties collectively rather than individually. It means analyzing how assets interact with one another in terms of risk, debt exposure, cash flow durability, tax positioning, and timing within the broader market cycle.

It shifts the question from:

“Is this property performing?”

to

“How does this property serve the portfolio as a whole?”

Many conversations in brokerage begin with valuation. Portfolio strategy begins with purpose.

When we review portfolios with owners, the first step is rarely pricing the asset. The first step is understanding what role each property should play in the portfolio.

In higher value, capital competitive markets like Orange County, portfolio level thinking often influences how consistently long term wealth compounds.

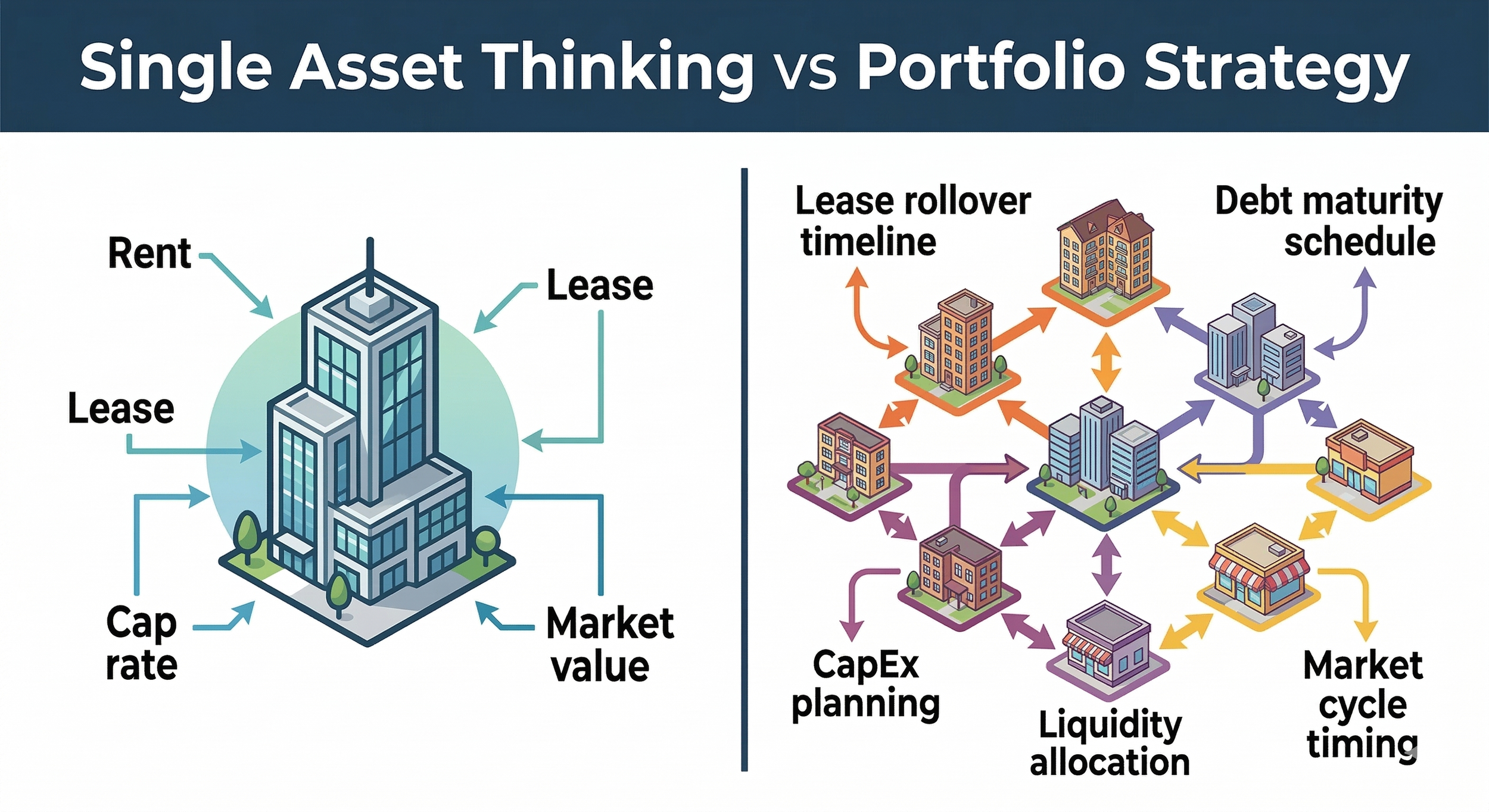

Single asset decisions focus on one property. Portfolio strategy evaluates how multiple assets interact across timing, risk, and capital allocation.

Definition of Portfolio Strategy in Commercial Real Estate

Portfolio strategy refers to the coordinated management of multiple commercial real estate assets to achieve long term financial objectives while managing risk across the entire ownership structure.

Rather than evaluating a property in isolation, portfolio strategy considers:

• Asset type diversification

• Geographic distribution

• Debt maturity schedules

• Lease rollover timing

• Tax exposure

• Liquidity position

• Market cycle positioning

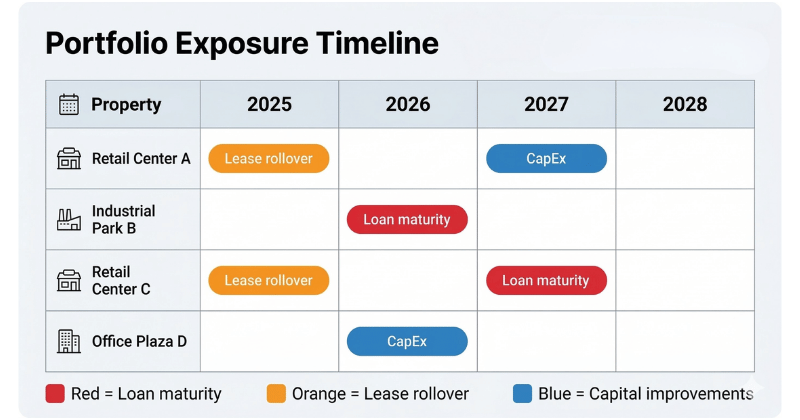

A single property might appear healthy on its own. But if three assets share similar lease expiration timelines, or multiple loans mature within the same year, portfolio risk may be elevated even if each asset individually looks stable.

Portfolio strategy is not simply owning multiple properties.

It is intentionally structuring those holdings to balance performance and risk over time.

How Portfolio Strategy Differs from Asset Management

Asset management focuses on maximizing the performance of a specific property. This includes leasing decisions, capital improvements, tenant retention, and operational oversight.

Portfolio strategy operates at a higher level.

Asset management asks:

How do we increase NOI at this building?

Should we renew this tenant?

When should we replace the roof?

Portfolio strategy asks:

Does this asset still align with our long term objectives?

Is this property increasing concentration risk?

Should we sell this asset to reposition capital elsewhere?

Are we overexposed to one sector?

For example, an Orange County owner may hold two retail centers and one industrial building. If retail rent growth slows while industrial demand strengthens, portfolio strategy may call for rebalancing even if both retail centers are stable.

Asset management optimizes performance within the property.

Portfolio strategy evaluates allocation across properties.

Ownership Patterns We Often See

Many Orange County owners did not set out to build portfolios intentionally. Portfolios often evolve organically over decades.

Common patterns include:

• Long held assets with low tax basis

• Portfolios that grew through opportunistic acquisitions rather than coordinated planning

• Clusters of loan maturities created during prior refinance cycles

• Deferred capital expenditures accumulating across multiple properties

Individually, each property may appear stable. But when these patterns occur across several assets simultaneously, risk exposure can increase.

Portfolio strategy helps owners identify these structural patterns early and sequence decisions before pressure points emerge.

Mapping lease expirations, loan maturities, and capital expenditures across multiple properties often reveals risks that are not visible when assets are evaluated individually.

Risk Balancing Across Multiple Properties

One of the core advantages of portfolio strategy is risk diversification.

In Orange County, ownership patterns often include:

• Long held retail centers acquired decades ago

• Family owned industrial buildings with low basis

• Mixed use developments with layered revenue streams

• Office properties that have faced vacancy challenges

Each asset type responds differently to economic cycles.

Retail assets tied to daily needs such as grocery anchored centers often provide stable traffic and long term tenants. Industrial assets respond to logistics demand and supply chain dynamics. Office performance depends on evolving workplace trends and tenant preferences.

If an owner concentrates heavily in one sector, portfolio volatility may increase.

Risk balancing may include:

• Combining stabilized income assets with growth oriented assets

• Diversifying across submarkets within Orange County

• Expanding outside the county to reduce geographic concentration

• Staggering lease expirations across multiple properties

Sophisticated owners intentionally avoid having all major leases expire within the same year. They also avoid structuring debt so that multiple loans mature simultaneously.

When downturns occur, diversification can help preserve liquidity.

Timing Decisions Across a Portfolio

One of the most overlooked components of portfolio strategy is timing coordination.

In Orange County, transaction volumes fluctuate based on interest rates, lending conditions, and buyer sentiment. When rates rise and financing tightens, transaction activity often slows. Owners who need to sell during those periods may face less favorable pricing.

Portfolio strategy anticipates these cycles.

Rather than reacting to an individual property’s issue, strategic owners may:

• Sell a property before major capital needs arise

• Refinance one asset to strengthen liquidity ahead of another loan maturity

• Use gains from a disposition to reduce leverage across the portfolio

For example, if two properties have loan maturities within 24 months, an owner may choose to sell the less strategic asset early to reduce refinancing pressure on the stronger property.

Single asset thinking reacts.

Portfolio strategy sequences.

Tax, Debt, and Liquidity Coordination

Portfolio strategy integrates tax planning and debt management into decision making.

In commercial real estate, tax exposure may include:

• Capital gains

• Depreciation recapture

• State tax considerations

If an owner sells a highly appreciated Orange County retail center, the tax impact can be significant. Portfolio strategy considers whether to:

• Execute a 1031 exchange

• Offset gains with losses elsewhere

• Stagger dispositions across multiple tax years

Debt coordination is equally important.

If several loans mature in a compressed period, refinancing risk increases. In a higher interest rate environment, refinancing may reduce cash flow. Portfolio strategy may include paying down debt on one asset using proceeds from another disposition to reduce overall leverage.

Liquidity planning also matters.

Owners with all capital tied up in stabilized properties may lack flexibility to pursue opportunistic acquisitions. Portfolio strategy seeks to balance income generation with capital flexibility.

How Advisors Model Portfolio Wide Decisions

Advisors who operate at a portfolio level use structured analysis that may include:

• Portfolio allocation snapshot (asset type, submarket exposure, tenant mix, lease duration)

• Rollover and loan maturity heat map (next 12–36 months)

• Capital plan forecast (CapEx requirements versus liquidity)

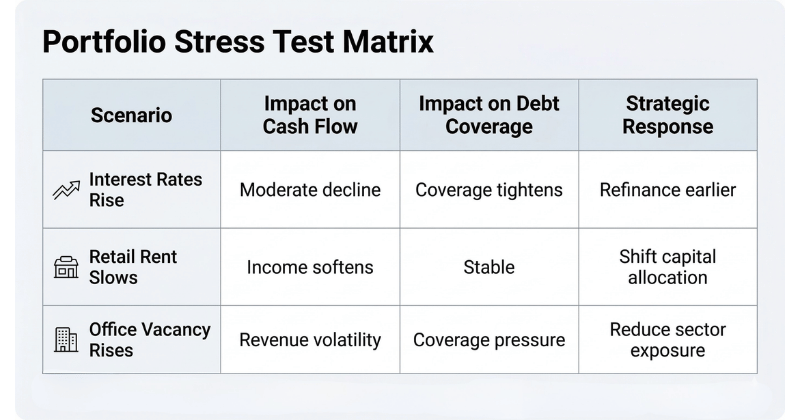

• Scenario testing (interest rate changes, rent growth shifts)

• Decision sequencing (sell, refinance, exchange, or acquire tied to owner objectives)

Rather than asking whether one asset should be sold, advisors test what happens if:

• The weakest performing asset is liquidated

• A 1031 exchange shifts exposure to a different sector

• Debt is reduced on one property to strengthen portfolio wide leverage

Modeling also includes downside scenarios.

What happens if retail rent growth slows?

What happens if office vacancy remains elevated?

What happens if financing spreads widen?

Portfolio level modeling replaces intuition with structured evaluation.

Sophisticated owners evaluate how market scenarios could influence portfolio performance before making disposition, refinance, or acquisition decisions.

Long Term Wealth Creation Through Portfolio Discipline

Commercial real estate wealth is rarely built through isolated decisions alone.

It compounds through allocation discipline.

Owners who think in portfolios often:

• Sequence transactions strategically

• Manage tax exposure intentionally

• Maintain liquidity flexibility

• Reduce sector concentration risk

• Position assets around long term objectives

Over decades, this discipline often produces more stable equity growth than reactive property level decision making.

Portfolio strategy is not about constant activity.

It is about clarity.

Conclusion

Portfolio strategy in commercial real estate means evaluating how assets work together rather than individually. It integrates risk management, tax planning, debt coordination, timing, and long term objectives into one framework.

In markets like Orange County where asset values are high and transaction margins are narrow, portfolio level thinking can produce more resilient long term outcomes than isolated decision making.

Owners who understand their holdings collectively are better positioned to:

• Navigate interest rate cycles

• Manage refinancing risk

• Preserve liquidity

• Protect long term equity

Single asset thinking optimizes today.

Portfolio strategy protects tomorrow.

The first step is rarely deciding whether to sell. The first step is understanding how the portfolio is structured.

Disclaimer

This article is provided for educational purposes only and does not constitute tax, legal, or financial advice. Commercial real estate decisions often involve coordination with CPA, legal, and financial advisors.